Term plans are the most affordable insurance coverage strategies. Term insurance coverage plans are pure risk plans in which the policyholder gets the full sum assured in case of death, else nothing. When you understand the quantity of cover that you need, you should do an online comparison of all readily available term insurance plans in terms of premium and functions. Unlike term insurance coverage, entire life plans offer you protection for the life time however at a much higher though set premium(payable for a pre-defined restricted period ). “If you are an individual in your 20s or 30s, a term strategy is the finest choice for you, however if you are a married individual with one or 2 kids, a mix of entire and term life represents a fantastic option.

We inform you why term plans are necessary, how much coverage you may need and things to keep in mind before buying one:

Understanding term Insurance

Term insurance plans are pure danger plans in which the policyholder gets the complete amount guaranteed in case of death, else nothing. It provides a high quantity of cover for an extremely little premium, which, on the death of the life guaranteed, is paid to the nominee. These plans offer protection for a given duration. In term insurance, there’s versatility in the mode of paying premiums. Either you can choose a routine premium payment option or a single premium payment. In regular payment, you have the alternatives of full-term routine payment or limited-term regular payment. In a limited-term routine payment, the protection is for a longer duration while you pay a regular premium just for restricted years. Even in the regular premium, you get different frequency alternatives as you can select, monthly, quarterly, yearly or semi-annual exceptional payment choices.

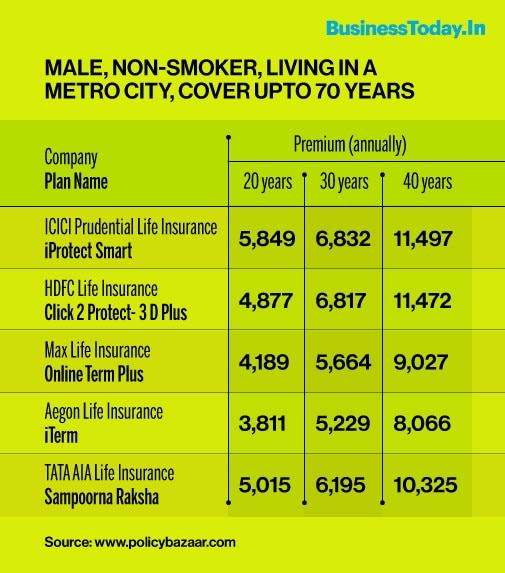

Which term plan to buy

Numerous kinds of term insurance coverage strategies are available in the market – level term insurance coverage, increasing term insurance coverage, term with return of premium (TROP), and reducing term insurance (likewise called home mortgage redemption).

Increasing term insurance coverage: The survivor benefit increases at set time periods but the premium stays the very same. It guarantees that the death advantage is changed for inflation due to the fact that household expenses even at the current worth will cost more in the future.

Decreasing Term Insurance: The sum ensured decreases every year with the same premium amount. These policies are available in useful when someone has big financial obligations and loans on them, says Santosh Agarwal, Chief Business Officer- Life Insurance, Policybazaar.com.

TROP Plans: In this strategy, if the insured passes away during the regard to the policy, the sum ensured is payable to the candidate, and if insured makes it through till maturity all premiums are returned.

Just how much cover you require

In insurance coverage, nobody size fits all. Premanshu Singh, CEO, Coverfox states leaping on the bandwagon of buying a Rs 1 crore term strategy is not a smart choice. The thumb guideline is to choose for a sum ensured that is 15-20 times one’s annual income. If a person has a yearly income of Rs 8 lakh, the perfect life cover for him will be in the range of Rs 8,00,000 x 15 (1.20 crore )and Rs 8,00,000 x 20 (Rs 1.60 crore), states Singh.

ALSO READ: Reliance Jio likely to get in mutual fund space, offer financial products through JioMoney

How to pick the very best plan

Umpteenth insurance plan are available in the market. Choosing a plan with the most affordable premium is not how it works. You must understand your requirements to pick the best-suited plan. Most significantly, the earlier you buy a term strategy, the better. The premium quantity increases as per the age, for that reason it is smart to buy a term plan prior to you hit 30 years of age.

{kind=link}